Newsletter SOLIFE Issue 9 | Q1 | 2022

Date

VERMEG certified SOC2 Type II

VERMEG has successfully completed a Service Organizations Controls (SOC) 2 Audit Type II examination as part of its continuing commitment to the security of customer data, and achieved an excellent score, with zero deviations reported.

Reaching this milestone is a result of the hard work and involvement of all departments in VERMEG.

SOC 2 audit and certification ensures VERMEG is storing, handling and transmitting while ensuring privacy, security, availability, integrity and confidentiality.

“Multi-Compartment” approach in life insurance

The Single Compartment approach can be summarized as defining multiple, different and independent products to address very specific customer needs. A more efficient alternative, the Multi-Compartment approach, is to build a more flexible overall product to better meet customer needs.

Needs on the “Customer” side

Taking out several life insurance plans has become an unavoidable reality for most policyholders for various reasons, including:

⁄ Changing needs & decision parameters over time: As customers go through various stages of life, their life insurance needs evolve. An individual’s investment profile and risk aversion can also change over time.

⁄ Evolution of available products: The range of life insurance products has expanded and evolved as a result of innovation (investment strategy, financial arrangements, financial instruments etc.) and changes to the regulatory framework.

Needs and Responses on the “Insurers” side

Dictated by customer needs most insurers have, so far, resorted to designing independent products (Single-Compartment approach), each responding to a specific need or a very limited subset of needs. However, this approach presents insurers with major limitations that can be summarized in the following points:

⁄ Excessive volume of policies managed at the portfolio level given multiple number of policies registered on the same holder;

⁄ Mobilization of significant operating resources (Human and material) in order to manage in most cases, redundant transaction processes related to their business system;

⁄ Products that lack transparency and flexibility for their owners.

“Multi-Compartments” management mode: also called Multi-Wallets or Multi-projects – combines “Customer” and “Insurer” interests.

The “Multi-Compartments” approach includes independent management of several investment modes /strategies (customer driven strategy, autopiloted strategy, company driven strategy or mandate strategy) within the same policy /product allowing:

⁄ Several investment strategies at the policy level (One strategy per investment coverage or per compartment or per project);

⁄ Specific risk coverages for each compartment.

The different compartments defined on a contract are autonomous in terms of coverage services (Regular addition or Regular withdrawal), investment services (automatic rebalancing, securing capital gains, progressive investment, etc.) and charges. The latter are manageable on a single policy in intra-compartment or inter-compartments or both.

Target representations of a product in “Multi-Compartments” management mode

In addition to meeting the expectations of the customer, the Multi-Compartments management mode:

⁄ Allows “Insurers” to extend their offerings to their customers and reduce their operating costs.

⁄ Avoids the “All or nothing” option for the saver

⁄ Allows a different investment portfolio, composed of appropriate assets for each compartment

⁄ Allows each “Saver” to take advantage of a single tax priority for all projects

VERMEG/SOLIFE – driving innovation in line with market expectations

VERMEG has integrated the “Multi-Compartments” management in SOLIFE during 2021. This integration has an impact on all product management parameters and is actually extending to all operations in the life cycle of a product/policy such as configuration of Multi-compartment products (creation and addition of compartments without limitation of number and according to the needs of the Insurer), investment processes (Subscription, Single Premium top up, Switch in…), divestment processes (Withdrawal, Switch out, transfer, Surrender, claim) and all technical or administrative endorsement (change of investment strategy, change of coverage or investment services, add a new compartment on policy…etc.).

User experience at the heart of digital transformation

The digital revolution, the increase in competition and the decline in the profitability of companies in the insurance sector are forcing them to undergo a profound digital transformation to enhance customer, employee and business or vendor partner experiences.

VERMEG’s Digital Transformation initiatives are in perfect synchronization with the expectations of insurers through the implementation of back-officer, individual life and collective digital journeys.

The digitization of insurance brokerage:

Competition from insurance companies and legal obligations requirements

Insurance brokerage companies have an interest in using the resources provided by the digitization of their activity to:

⁄ simplify the accomplishment of the multiple administrative tasks they are responsible for;

⁄ ensure their commercial development in the face of increasing competition, equipped and digital (Proximity brokerage );

⁄ comply with the new regulatory obligations that weigh on the entire profession (directives relating to the distribution of insurance products and the protection of personal data );

⁄ face the competition from start-ups offering easier online onboarding across an increasingly wide range of contracts;

⁄ adapt to the digital transformation which continues to progress among their main partners: the insurance companies.

The quest for digital transformation is driving significant spending on enabling technologies and services. In fact, just a year ago, IDC (International Data Corporation) forecasted that worldwide spending on digital transformation is expected to reach $1.97 trillion by 2022.

Digitally Transform Insurer Back-Office Operations:

Go Digital to Streamline Operations

When an insurance company digitally transforms its front-end systems and fails to do so with its back office, it’s fostering a disconnect that can impact company-wide communication and the customer experience, hold back productivity, and inhibit innovation and scalability. Areas to focus on:

⁄ Digitally enable processes to enhance employee experiences help streamline product development and key functions like claims and underwriting ;

⁄ Re-engineer the mailroom through digital transformation. Once made digital, mail assets can be analyzed to determine their level of importance and routed to the appropriate department or person to best handle the correspondence.

A large part of the back-office manager’s tasks could disappear with the deployment of automated solutions. Thus, the performance of checks (which involve numerous manipulations), the management of compliance and the risks associated with the products and services offered leaving more space to the resolution of problems, complex or unprecedented, not resolved by the automated solution and requiring the intervention of a specialist.

Insurance Customer Experience :

How an Insurance Self-Serve Portal Can Enhance Customer Experience?

For the insurance industry many modern customer service strategies involve self-service Portal. A customer service portal enables users to :

⁄ Find their own solutions by creating an easily accessible and navigable knowledge base, insurance companies can empower their customers by providing answers to their most frequently requests. Research shows that most customers begin by searching for an answer online before they contact customer support;

⁄ Make it easier for customer to register a claim and keep a tab on it (faster processing, automated claims process, better coordination amongst multiple parties, easier to check claim status etc.);

⁄ Receive payment without waiting on hold or in queue to be answered by an insurance representative;

⁄ Have 24/7 Access to Services.

VERMEG’s Digital Transformation initiatives

VERMEG is focused on its areas of expertise to deliver differentiating, normalized and customized journeys to meet insurer and broker challenges.

VERMEG is focused on its areas of expertise to deliver differentiating, normalized and customized journeys to meet insurer and broker challenges.

The digitization of insurance brokerage and back officer journeys :

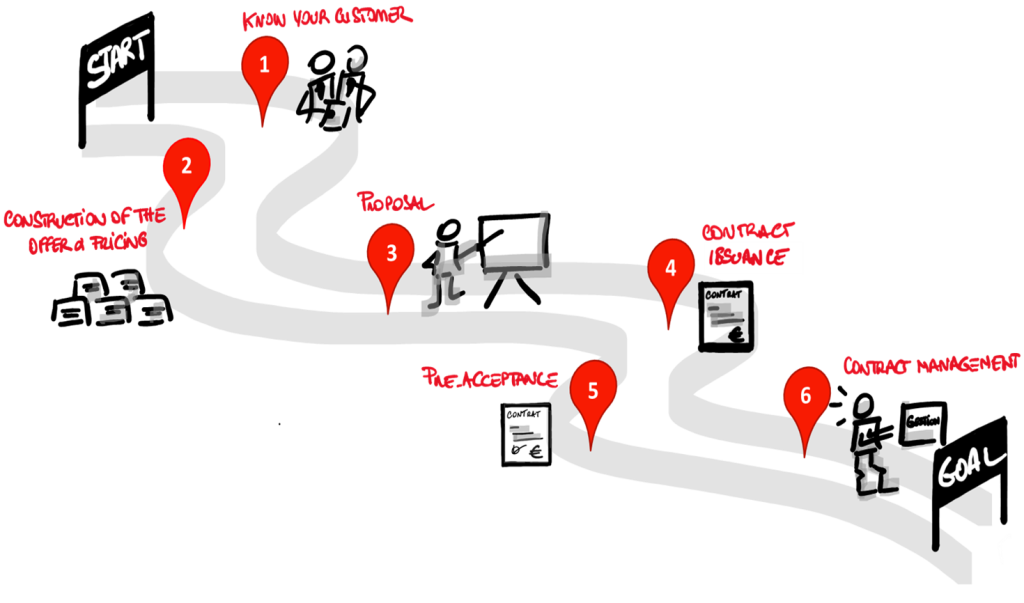

VERMEG offers a seamless end-to-end approach with 5 key steps around a business process (from onboarding to contract management) that meets the needs of all stakeholders.

The scope of the digitization of insurance brokerage and back office journey includes:

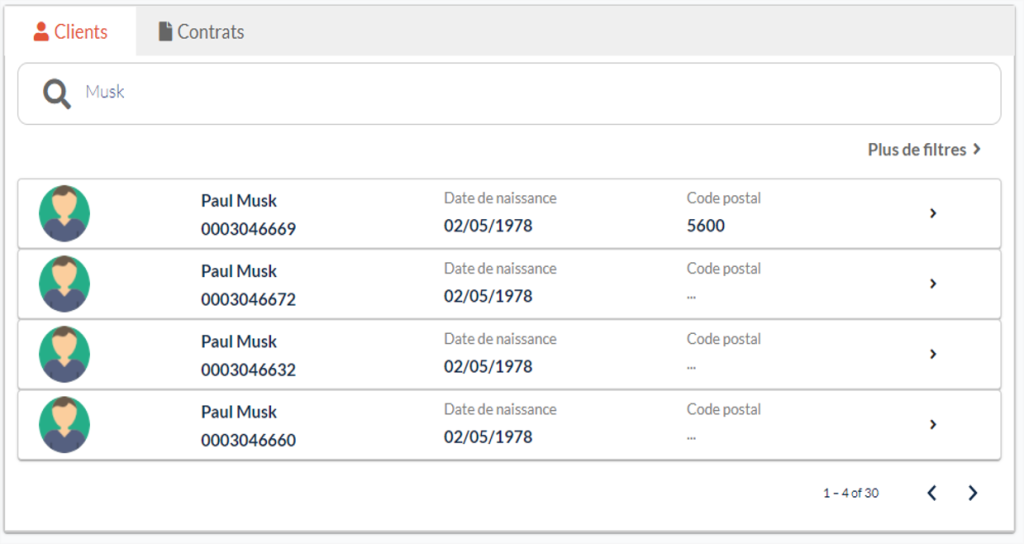

⁄ The 360° view of customer;

⁄ Construction of the offer, pricing and proposal;

⁄ Contract issuance and pre-acceptance (subscription);

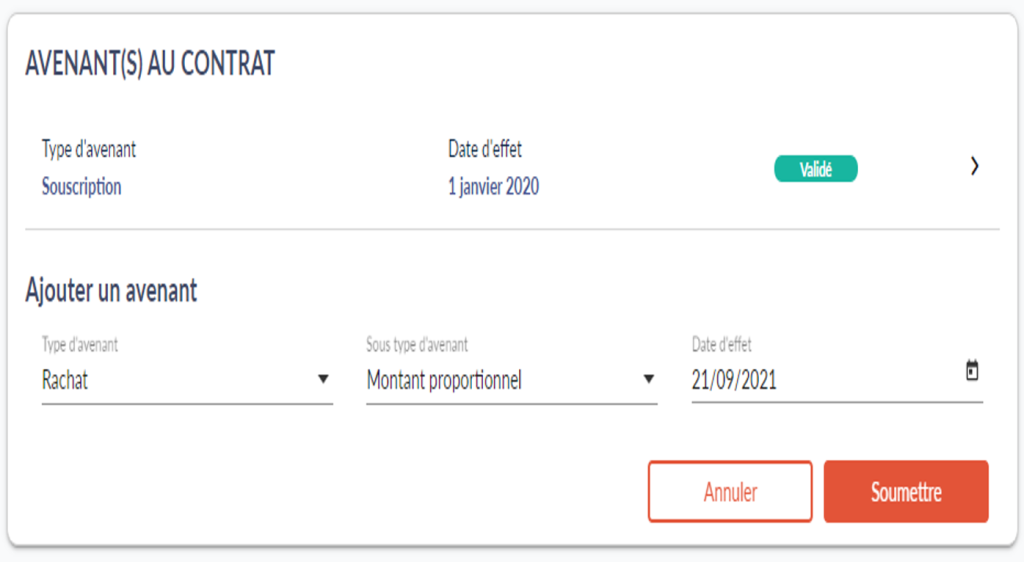

⁄ Contract management (all kinds of endorsement: switch, withdrawal, surrender etc.);

⁄ The GAC module : “competitor endorsement management” module.

Download the Newsletter